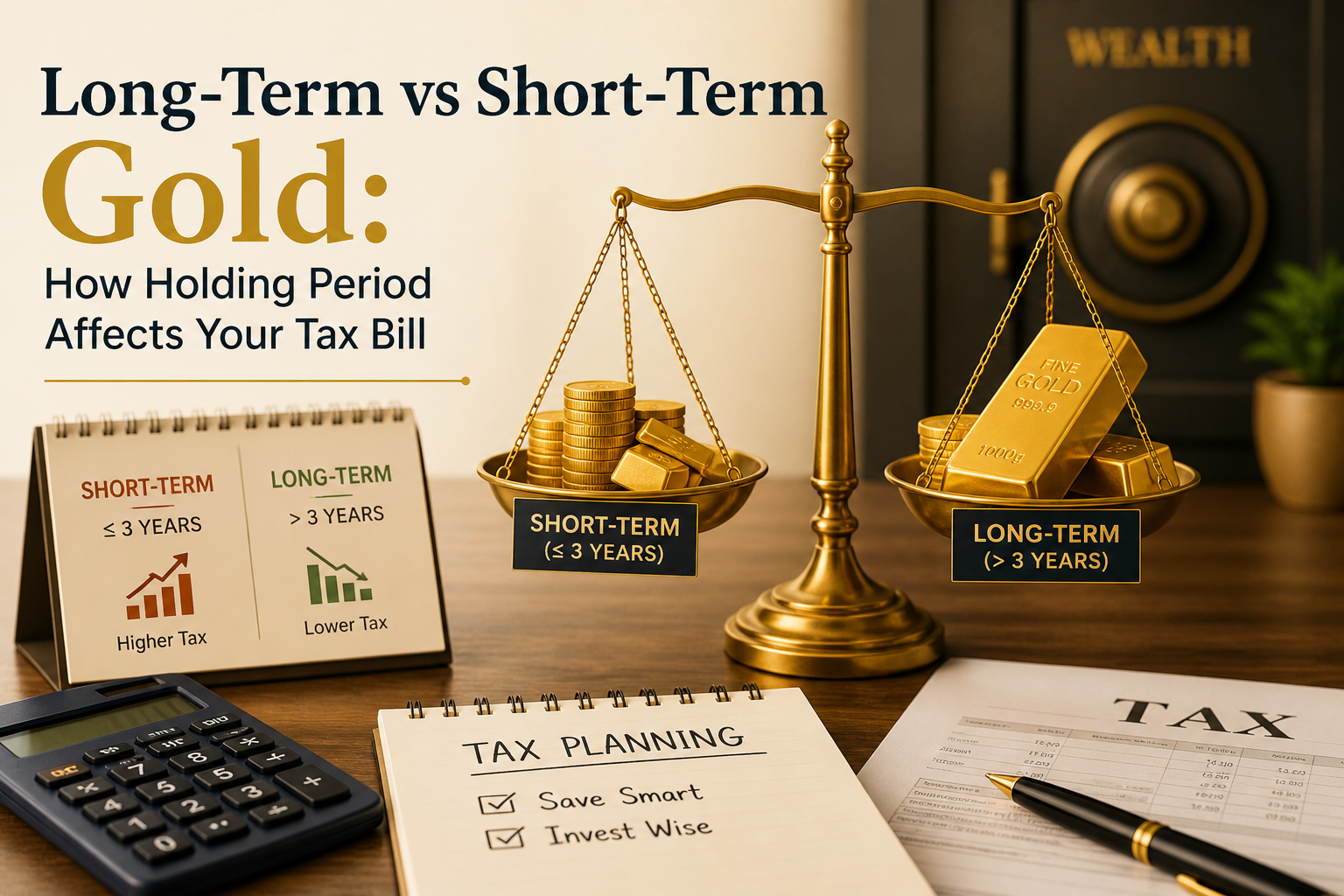

How STCG on Gold Is Taxed

Short-term capital gains on gold — arising from gold held for 24 months or less — are treated as ordinary income. They are added to your total income for the year and taxed at your income tax slab rate. For a person in the 30% tax bracket, a ₹50,000 short-term gain on gold would attract ₹15,000 in income tax (plus applicable surcharge and cess).

For lower-income individuals (total income below ₹3 lakh), even short-term gains from gold attract zero tax under the basic exemption limit. For those in the 5% slab (income ₹3–7 lakh), the tax on a small short-term gold gain is modest. The burden is most significant for the 20% and 30% slab taxpayers, who have the strongest incentive to hold past the 24-month threshold.

How LTCG on Gold Is Taxed

Long-term capital gains on gold (held more than 24 months) are taxed at a flat 12.5% on the gain, regardless of the seller's income level or tax bracket. This flat rate applies uniformly — a 30% bracket taxpayer and a 20% bracket taxpayer pay the same 12.5% on LTCG from gold. There is currently no indexation benefit for gold LTCG under post-2024 Budget rules.

The flat 12.5% LTCG rate is advantageous for anyone in the 20% or 30% income tax bracket. For those in the 5% bracket, STCG might actually result in a lower effective tax rate (5%) than LTCG (12.5%) — an unusual situation where holding past 24 months could increase the tax bill for low-income sellers.

Practical example: Gold bought in September 2023 for ₹60,000, sold in August 2025 (23 months later) for ₹72,000. Gain = ₹12,000. STCG at 30% slab = ₹3,600 tax. If sold in October 2025 (25 months later, LTCG): ₹12,000 × 12.5% = ₹1,500 tax. Waiting just 2 months saves ₹2,100. For a 50-gram lot, the saving on the same percentage gain would be ₹10,500+.

How Timing Your Sale Can Reduce Tax

For gold holders approaching the 24-month mark, checking the exact purchase date and counting to the sale date is a worthwhile exercise. The holding period is calculated in calendar months from the date of purchase to the date of sale. If you are at 22 months and planning to sell, waiting two more months — if your financial situation allows — moves you into LTCG territory and reduces the tax rate from your slab rate to 12.5%.

This timing benefit is worth quantifying with your specific numbers. The larger the gain and the higher your income tax bracket, the more valuable the LTCG classification becomes. For small gains or those in the 5% bracket, the difference may not be worth the wait. For large lots or high-income sellers, a 2–6 month delay at the right moment can represent a tax saving of tens of thousands of rupees.

Tags